Why the Wealthiest Families Don’t Just Invest — They Architect

The case for a hybrid asset strategy, and why PPLI changes everything

Most wealthy families don’t lose their wealth because they made bad investments. They lose it because they never built the right structure around those investments. A growing consensus among family offices confirms that the future of asset management is hybrid — liquid and illiquid, public and private, active and passive, across geographies and generations. But there is one dimension most of these discussions overlook entirely: the container matters as much as the contents.

This is where Private Placement Life Insurance (PPLI) enters the picture — not as an insurance product, but as the strategic architecture layer that makes a hybrid family strategy fully operational. PPLI is available only to qualified or professional investors under applicable regulation and is not suitable for all jurisdictions or investor profiles. Its power lies precisely in that sophistication.

The Stakes Have Never Been Higher

Three data points from 2025 set the stage for why structural wealth planning is no longer optional for internationally mobile families:

According to Cerulli Associates’ June 2025 report, UHNW and HNW households — just 2% of all households — will account for over $62 trillion of these transfers. The UBS Global Family Office Report 2025, drawing on 317 family offices with an average net worth of $2.7 billion, confirms that geopolitical risk, cross-border complexity, and succession readiness are now the defining concerns of sophisticated wealth holders. Yet the gap between intention and structure remains vast: while 69% of North American family offices report having a succession plan, only around 30% of those are formal written documents (RBC/Campden Wealth North America Family Office Report, 2025).

The wealth is there. The intention is there. The architecture, too often, is not.

1. The Hybrid Strategy: What It Looks Like Without PPLI

A typical ultra-high-net-worth family today holds assets across four buckets:

Liquid public markets — equities, fixed income, ETFs

Alternative investments — private equity, venture capital, hedge funds

Real assets — real estate, infrastructure, commodities

Cash and liquidity reserves

According to the UBS Global Family Office Report 2025, the average family office today allocates 26% to developed market equities, 21% to private equity, 10% to real estate, and 26% to fixed income — a genuinely hybrid posture. The investment strategy is sophisticated. The structural architecture surrounding it, in most cases, is not.

Without the right container, four silent destroyers erode wealth year after year:

Annual tax drag — the silent 30% haircut

In most high-tax jurisdictions, capital gains taxes of 25–33% make the cost of managing a hybrid portfolio without deferral substantial. (Note: some jurisdictions such as Switzerland impose no capital gains tax on private investors; the impact varies materially by domicile.) It is worth noting, however, that Swiss tax authorities may reclassify individuals who trade with significant frequency or leverage as professional securities dealers, in which case gains become subject to income tax — a distinction that underscores the importance of obtaining jurisdiction-specific tax advice before assuming favourable treatment. Consider an illustrative calculation: a family investing €10M at 8% gross annual return, in a fully taxable, actively rebalanced scenario with 25% tax on gains each year, nets an effective after-tax return of approximately 6% per annum. Over 20 years, that produces roughly €32M.The same portfolio with full tax deferral — such as inside a PPLI wrapper — compounds at the full 8%, reaching approximately €46.6M. A gap of nearly €14.6M: not from better investments, but purely from structure.

Cross-border complexity that multiplies costs

Wealthy families rarely live in one country. Assets in Luxembourg, beneficiaries in the UK, a trustee in Switzerland, a holding company in Dubai — each layer adds reporting obligations, potential double taxation, and legal uncertainty. Various industry studies suggest that operating and compliance costs for complex, cross-border family office structures often consume 0.3–0.8% of AUM annually — a drag that compounds as destructively as any market drawdown.

Estate transfer: expensive, slow, and accelerating

Without structuring, transferring assets at death triggers estate taxes — up to 40% in the UK under current Inheritance Tax rules, up to around 40% federally in the US (before any additional state-level estate or inheritance taxes), and up to 45% in Germany depending on the beneficiary relationship — alongside probate proceedings averaging 12–18 months and potential forced liquidation of illiquid positions at precisely the wrong moment. With Cerulli Associates projecting $124 trillion in global wealth transfers through 2048, and UBS reporting that heirs inherited a record $297.8 billion in 2025 alone — up 36% year-on-year — the structural cost of poor estate planning is compounding in real time.

Governance breakdown across generations

The RBC/Campden Wealth North America Family Office Report 2025 found that while 69% of family offices now have a succession plan — up from 53% the prior year — only around 30% of those plans are formal written documents. The Bank of America 2025 Family Office Study (335 family offices, surveyed May–June 2025) found that one in three expect to transition control within the next five years. When assets are held in fragmented structures without a unifying governance logic, this wave of transitions becomes a risk event, not a milestone.

2. What is PPLI?

Private Placement Life Insurance is a bespoke life insurance policy — typically issued in Luxembourg, Liechtenstein, Ireland, or the Cayman Islands — where the policyholder’s assets are held within an insurance wrapper and managed by a chosen investment manager. The legal form is insurance. The economic function is a tax-efficient, multi-asset holding vehicle for sophisticated investors.

Key structural features:

Eligible investors: qualified or professional investors only (UHNW individuals, family offices, institutional clients)• Minimum premium: typically €1–5M+ depending on provider and jurisdiction (select platforms from €500K)

Eligible assets: equities, bonds, private equity funds, hedge funds, real estate funds, structured products — subject to diversification and investor control tests

Jurisdictions: Luxembourg (most common in EU), Liechtenstein, Ireland, Cayman Islands (for non-EU clients)

Regulatory framework: EU Insurance Distribution Directive (IDD), local insurance supervision; CRS/FATCA reporting applies

A note on investor control and diversification tests: Regulatory requirements in most PPLI jurisdictions impose limits on the degree of control a policyholder may exercise over underlying assets and mandate diversification across securities. These tests preserve the insurance character of the policy and therefore its tax treatment. Structuring that respects these boundaries — rather than seeking to circumvent them — is what distinguishes a durable PPLI architecture from a fragile one.

3. The Same Strategy with PPLI: A Different World

Tax-deferred compounding — the structural alpha

Assets inside a PPLI policy grow free of income tax and capital gains tax for as long as the policy is in force. Returning to our illustrative scenario: €10M compounding at 8% gross over 20 years inside a PPLI structure reaches €46.6M, versus approximately €32M in a fully taxable, actively rebalanced account with 25% annual tax on gains. The wrapper alone contributes nearly€14.6M of additional outcome — without taking a single additional unit of investment risk.

Full investment flexibility — the wrapper follows the strategy

Unlike retail insurance products, PPLI allows investment into virtually any asset class: private equity funds, hedge funds, fixed income, real estate, structured products. The UBS GFO 2025 confirms that family offices are shifting toward developed market equities and private debt; a PPLI wrapper accommodates precisely this kind of dynamic, multi-asset allocation. Leading platforms in Luxembourg offer access to hundreds — in some cases well over a thousand — approved funds, including most major private equity and hedge fund managers.

Seamless generational transfer — outside probate

Life insurance proceeds transfer to named beneficiaries outside probate and, in many jurisdictions, free of inheritance tax. With the RBC/Campden Wealth 2025 report finding that nearly half of all North American family offices expect a generational transition within the next decade, the ability to transfer assets within weeks rather than 18 months — without court involvement or forced liquidation — has never been more operationally relevant.

Cross-border portability — the EU passport advantage

PPLI structures issued in Luxembourg under the EU’s insurance passport framework are recognised across all EU member states, subject to local tax treatment in the policyholder’s jurisdiction of residence. For mobile families — or those planning a change of domicile — this is amaterial advantage over holding companies or trusts, which often face hostile recharacterisation when the family moves.

Asset protection — a legal firewall

In many jurisdictions, assets held within life insurance contracts, including PPLI, benefit from strong protection vis-à-vis both the insurer’s creditors and, in many cases, the policyholder’s own creditors — subject to local law and applicable clawback rules. In Luxembourg, this is reinforced by the Insurance Contract Law and the ‘Triangle of Security’ regime, which grants policyholders a super-privilege over the insurer’s ring-fenced assets.

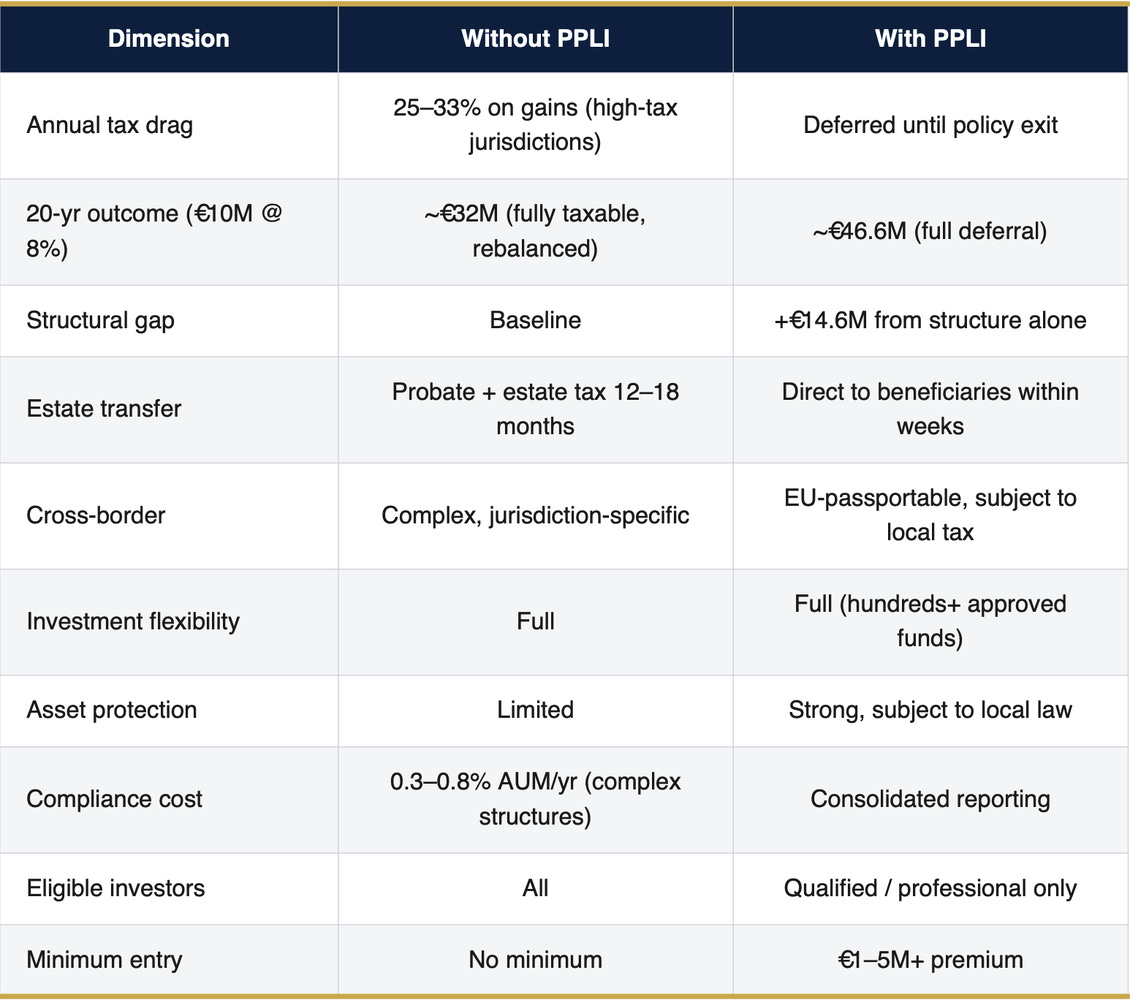

4. Head-to-Head Comparison

All figures illustrative only. Compounding example assumes 8% gross annual return and 25% flat annual tax on gains for the non-PPLI scenario; no additional costs included. Actual outcomes depend on jurisdiction, individual tax treatment, asset allocation, and investor circumstances.

5. Illustrative Scenarios: The Difference Structure Makes

The following are illustrative scenarios designed to demonstrate the structural principles discussed. They do not represent specific clients or guaranteed outcomes.

A German tech founder sells his company for €15M. Proceeds are placed into a personal investment account at a private bank, invested across equities, private equity funds, and fixed income — an effective hybrid strategy, but held in a plain taxable structure.

Assuming 8% gross return with 25% annual tax on gains (~6% net effective return), the portfolio reaches approximately €20.1M after five years. Cumulative tax events from rebalancing total an estimated €1.3M over that period. The estate plan relies on a German will requiring notarial probate — estimated at €180,000+ and up to 9 months of proceedings. Two of his three children reside in France and the UK, creating cross-border inheritance complications.

Projected structural cost over 20 years: €10–15M in foregone compounding, estate costs, and cross-border friction.

The same founder structures his exit proceeds into a Luxembourg PPLI policy before the sale closes. The identical investment mandate is replicated inside the wrapper using the same private bank as investment manager, in full compliance with Luxembourg diversification and investor control tests.

Rebalancing and fund switches within the policy trigger no taxable events. After five years at the full 8% gross, the portfolio reaches approximately €22.0M — approximately €1.9M more than Scenario A, purely from tax deferral. The policy names his three children as beneficiaries across jurisdictions; on death, proceeds transfer outside German probate, saving an estimated €200,000+ and 9 months. The Luxembourg EU passport means the structure remains intact if he relocates, subject to local tax treatment.

Estimated advantage over 20 years vs. Scenario A: €12–18M in additional net wealth — from the same underlying investments.

A Middle Eastern family office manages €80M across four asset classes, with an asset allocation broadly in line with the UBS Global Family Office Report 2025 averages: developed equities, private equity, real estate, and fixed income. Operating and compliance costs for its complex cross-border structure average approximately 0.5% of AUM annually (€400,000/year). Estate planning relies on offshore trusts from the 1990s, increasingly challenged by OECD transparency initiatives (CRS, BEPS).

A €30M sleeve is restructured into a Luxembourg PPLI policy. Within 18 months, consolidated reporting replaces three separate compliance streams. Tax drag on the restructured sleeve is eliminated during the accumulation phase. The policy is recognised across the four EU countries where family members reside, subject to local tax treatment in each jurisdiction. With the RBC/Campden Wealth 2025 data showing that nearly half of family offices expect a generational transition within a decade, the family has also begun designating the next generation as primary beneficiaries under the policy.

Illustrative outcome: €150,000–290,000/year in compliance savings on the restructured sleeve, plus a significantly enhanced compounding trajectory aligned with the family’s 20-year wealth preservation mandate.

6. What Sophisticated Families Are Actually Doing

The UBS Global Family Office Report 2025 confirms that family offices are increasingly institutionalising their approach: shifting toward active management, diversifying into private debt, and prioritising succession readiness. Yet the same report shows that most are doing so without a unifying structural layer. The most forward-thinking offices are changing that:

A PPLI policy as the core wrapper, holding a diversified portfolio of funds and direct investments aligned with the family’s strategic asset allocation

A family investment policy statement governing asset allocation, risk parameters, and rebalancing rules

A multi-generational mandate with clearly designated beneficiaries and formal governance protocols — addressing the gap identified in the RBC/Campden Wealth 2025 report

Complementary structures (foundations, holding companies) for operating assets that cannot sit inside the PPLI wrapper

This is no longer the preserve of dynastic wealth. As minimum premiums have become more accessible and PPLI platforms have expanded, families with investable assets of €3M and above can access structures once reserved for the top 0.01%.

Conclusion

We are living through the largest intergenerational wealth transfer in history. Cerulli Associates projects $124 trillion changing hands globally through 2048, with UHNW households — just 2% of families — driving over half of that volume. The families that preserve and grow their share of this transfer will not necessarily be the ones with the best investments. They will be the ones with the best architecture.

A hybrid investment strategy gives you the right ingredients. PPLI gives you the right container. Without both, you are leaving a significant portion of your family’s financial legacy on the table — not through bad decisions, but through structural neglect.

The families who understand this distinction are the ones who stay wealthy across generations. The data from 2025 makes the case more clearly than ever before.

Key sources: UBS Global Family Office Report 2025 (317 family offices, avg. net worth $2.7B, conducted Jan–Apr 2025); RBC Wealth Management / Campden Wealth North America Family Office Report 2025 (141 family offices, avg. total wealth $2B); Bank of America 2025 Family Office Study (335 family offices, May–Jun 2025); Cerulli Associates, ‘U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2024’ / Great Wealth Transfer projections (June 2025); UBS Billionaires Ambitions Report 2025.

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. PPLI is not suitable for all jurisdictions or investor profiles; suitability depends on individual circumstances, domicile, and applicable regulation. All numerical examples are illustrative and based on simplified assumptions; actual outcomes will vary. Compounding examples assume 8% gross annual return with 25% flat annual tax on gains for the non-PPLI scenario; no additional costs are included. Tax and estate planning laws are subject to change. Consult your independent legal, tax, and financial advisers before making any structural decisions. All figures in euros unless otherwise stated.

My LinkedIn: DoboshOfficial